Key Takeaways:

-

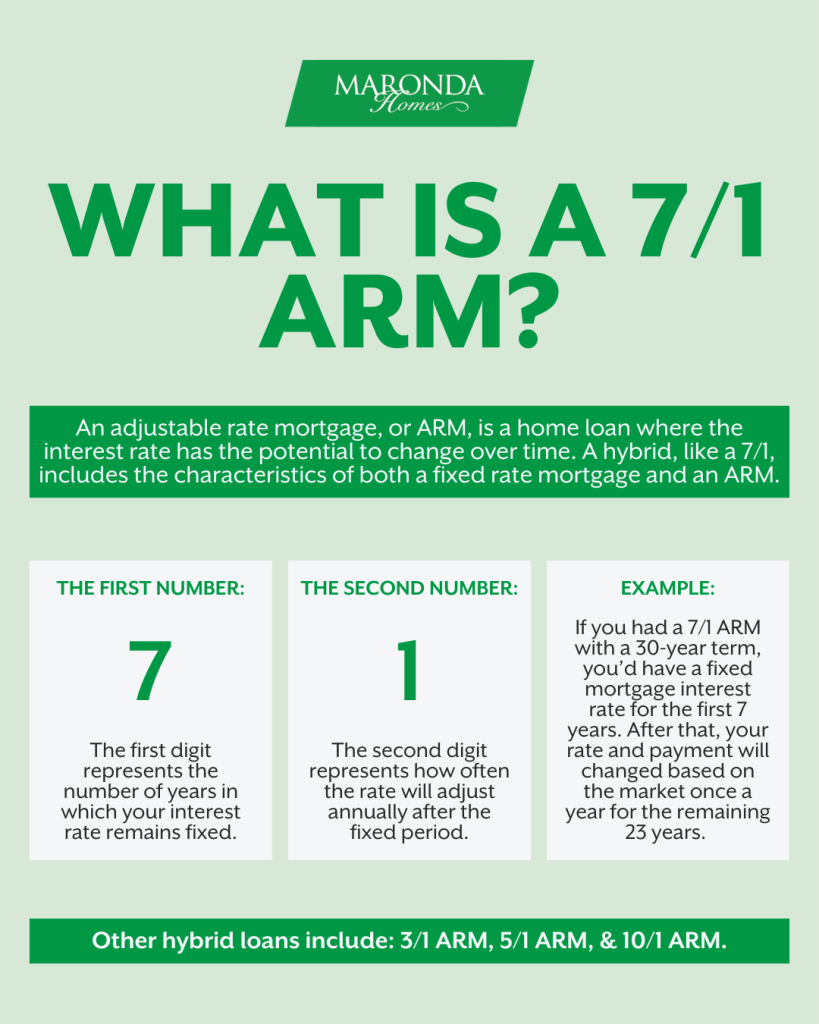

ARMs often start with a fixed interest rate for a set number of years. For example, a 7/1 ARM maintains a fixed rate for the first seven years before adjusting annually.

-

After the fixed period, the interest rate adjusts based on a specified index plus a margin. This means your monthly payments can increase or decrease, depending on market conditions.

-

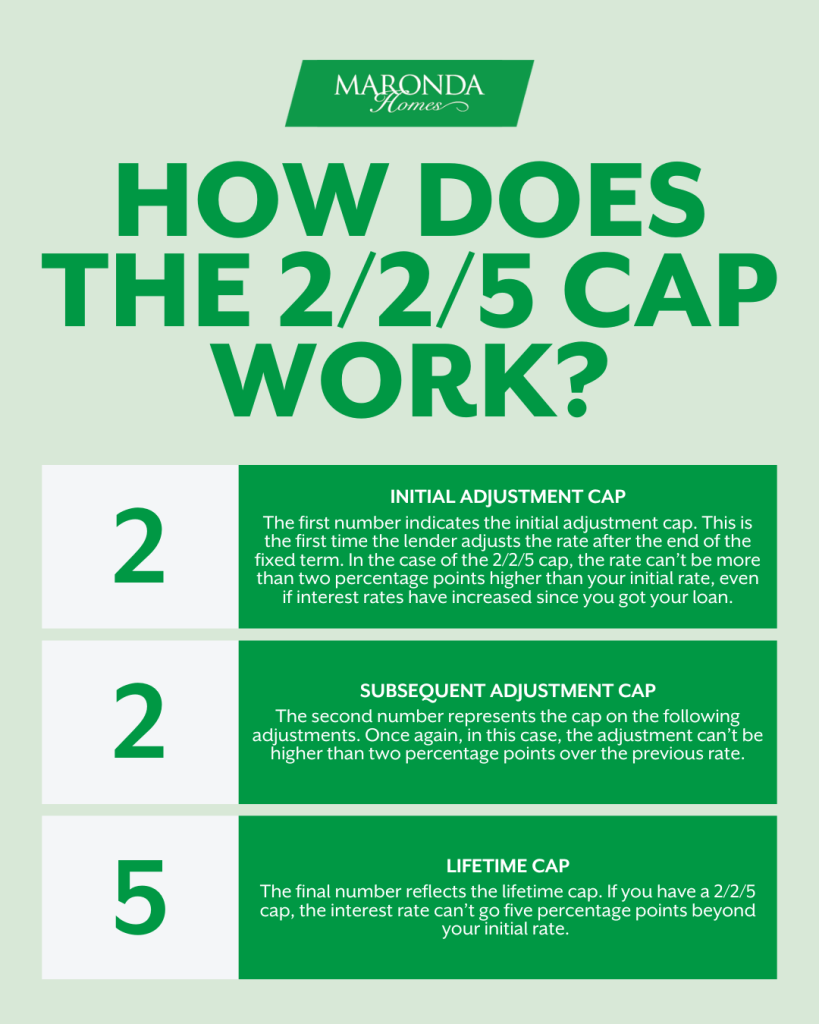

ARMs typically include caps that limit how much the interest rate can change at each adjustment and over the life of the loan. A common structure is a 2/2/5 cap, meaning a 2% limit on the initial adjustment, a 2% limit on subsequent adjustments, and a 5% lifetime adjustment cap.

-

ARMs may be suitable for borrowers who plan to sell or refinance before the adjustable period begins, potentially benefiting from lower initial rates. However, they carry the risk of increased payments if interest rates rise.

What is an Adjustable Rate Mortgage?

Commonly referred to as an “ARM”, an adjustable-rate mortgage is a home loan where the interest rate has the potential to change over time. Some ARMs are hybrids, which means a lower fixed rate will be offered for a set period of time.

What are the different types of Adjustable Rate Mortgages?

One of the most attractive and popular Adjustable Rate Mortgages is the 7/1 ARM. For the first seven years of the mortgage, the loan operates as a fixed-rate mortgage. After the seven-year period, the rate adjusts according to the market.

How does an ARM work?

ARMs correlate directly with the market and adjust over time after your initial fixed-rate period. You could end up with a lower monthly payment if rates fall, or a higher monthly payment if rates rise. They’re designed to adjust yearly to ensure that your mortgage is paid off on time.

The adjustable-rate is determined by the index, which represents a market rate, and the margin applied to the market rate. After your fixed-rate period, your lender will review market rates, add the margin to the index, and automatically adjust your payment for you.

Although your mortgage rate adjusts regularly after the initial fixed period with a 7/1 ARM, there are caps on how high it can go. The most common cap used is the 2/2/5.

Is an ARM Right For You?

One of the biggest pros to a 7/1 ARM is the lower initial rate. Your mortgage payments will be low during the first seven years of your loan. This type of loan is typically used for homeowners that are planning to refinance or pay off the loan prior to the expiration of the introductory rate.

7/1 ARMs can also be a smart option for homebuyers who plan to move within seven years. Once the seven-year fixed period is up, you could save money by selling the house before the rate adjusts – especially if interest rates have risen.

One of the most important things to recognize with a 7/1 ARM is that your payments correlate with the market after the seven-year fixed rate. If rates drop, you could end up paying less in mortgage expenses, but if they continue to rise, you could end up paying more mortgage expenses.

Although the type of loan is fairly flexible, it can be complex. Some have complicated rules, fees, and structures. If you’re interested in a 7/1 ARM, be sure to ask your lender about prepayment penalties and other details of importance.

Today’s ARMs are different from the ARM loans from the early 2000s. Arms today are better regulated than those that originated in 2008.

“The newer regulations cap rate adjustments, which limit percentage increases per period and over the life of the loan, minimizing the risk of payment shock that homebuyers may experience,” Brian Rugg, chief credit officer at loanDepot, told Yahoo Money. “Credit and income criteria have also become more restrictive, which enables lenders to validate that an ARM will be an affordable, long-term solution for their borrowers.”

At Maronda Homes, our preferred lender is there to help navigate you through the loan process. From learning your wants and needs to discussing which mortgage is right for you, they’ll be with you every step of the way.